Alternative Underwriting's Moment of Truth

The macro cycle will show us what's viable, and what isn't

My credit career started in 2005. Back then, it seemed easy to underwrite risky credit. The lending decisions we made turned out to be right almost every time. But my boss at the time cautioned me against trusting my expertise too much. He warned:

In good markets, it’s impossible to tell who’s good at this and who isn’t, because everything works. When the market turns, when everything stops working - that’s when we’ll find out who’s actually good at this.

A few years later, the 08-09 cycle showed us who was actually good at credit.

The last decade has brought new entrants, new technologies, and new strategies in the consumer underwriting space. The aim of many of these entrants was to outperform traditional methods that we use for everything from auto loans to personal credit cards. They certainly grew loan volumes. But did that volume come at a cost of excess credit losses?

The answer is - we’re about to find out. Years of relatively benign credit conditions are turning in 2023, and now macro stresses will show us which new strategies actually work through a cycle, and which were just a product of the environment. So, how will we judge what worked and what didn’t?

Conventional products can provide a benchmark. For unsecured consumer credit, let’s start with historical credit card charge-offs1:

A few things to note:

Recessionary periods (shaded gray) coincide with increased charge-off rates.

Charge-off rate increases range from +2.0% to +3.0% excluding ‘08-09 (+7.5%).

2020 did not look like a typical recession; future cycles won’t look like 2020.

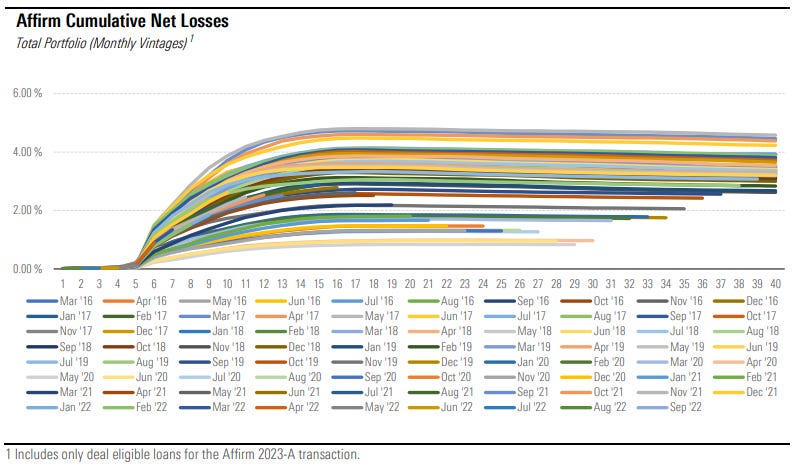

These points of reference inform how we might expect alternative underwriting methods to perform through a cycle. While not all alternative underwriters have published information that we can track, there are some public data points for their brief history. Take a look at the cumulative loss rates for a prominent BNPL player, Affirm2:

If you cut through the headline noise, you can see two things:

Net loss rates (as a directional proxy for charge-off rates) are comparable over the past several years to credit cards. In fact, vintages from 2020 and later trended below 2% just like credit cards did.

The historical look-back period includes one recessionary period (2020).

The data provides a bit of a Rorschach test. For optimists, you can see alternative underwriting’s comparable performance despite reaching “down” what we see as the traditional credit spectrum. For skeptics, you can see a sobering lack of historical track record through any prior cycle - and no, 2020 didn’t really “count” as a credit cycle. So who’s right, the optimists or the pessimists?

I think good alternative underwriting will perform in line or better than traditional methods during this credit cycle. Alternative underwriting, using the right data, yields a better real-time picture of credit risk than traditional methods. Closed-end loans (like BNPL) re-underwrite the borrower for each transaction, as opposed to open-ended revolving credit (read: traditional credit cards). These features SHOULD sharpen the underwriting decision and avoid excess credit losses. But as the market is showing us, some new market participants are already struggling to manage their credit losses3.

When the dust settles, the performance of credit models in 2023 will show us, in the words of my old boss, “who’s actually good at this.” And that’s how we’ll know which credit underwriting models we should trust in the years to come.

The Efficient Frontiers is written by James Chemplavil and Ryan Barrett, the co-founders of Salus, a digital underwriting platform. It will tell you what we’re thinking about, what we’re doing, and where we’re going next. We want to hear from you, so reach out to us at info@salusfintech.com to take a deeper dive. Thanks for coming on this journey with us.

“Charge-off Rates on Credit Card Loans, All Commercial Banks.” Federal Reserve Economic Data (FRED). https://fred.stlouisfed.org/series/CORCCACBS

“Affirm Asset Securitization Trust 2023-A, Rating Report.” Morningstar DBRS, January 2023.

“Varo’s Losses Shrink but Growth Stalls: Q4 Call Report.” Fintech Business Weekly, February 2023.